Unveils Upgraded Token with Exclusive Presale Opportunity!")

The difficulty of mining a bitcoin block fell by 7.32% today, with miners powering off machines as a brutal bear market eats into profit.

The adjustment at block height 766,080 is the biggest downward change since July 2021, data from mining pool BTC.com shows. That was when hordes of miners dropped off the network following China’s ban on the industry. At the time, the country was the world’s biggest bitcoin mining hub.

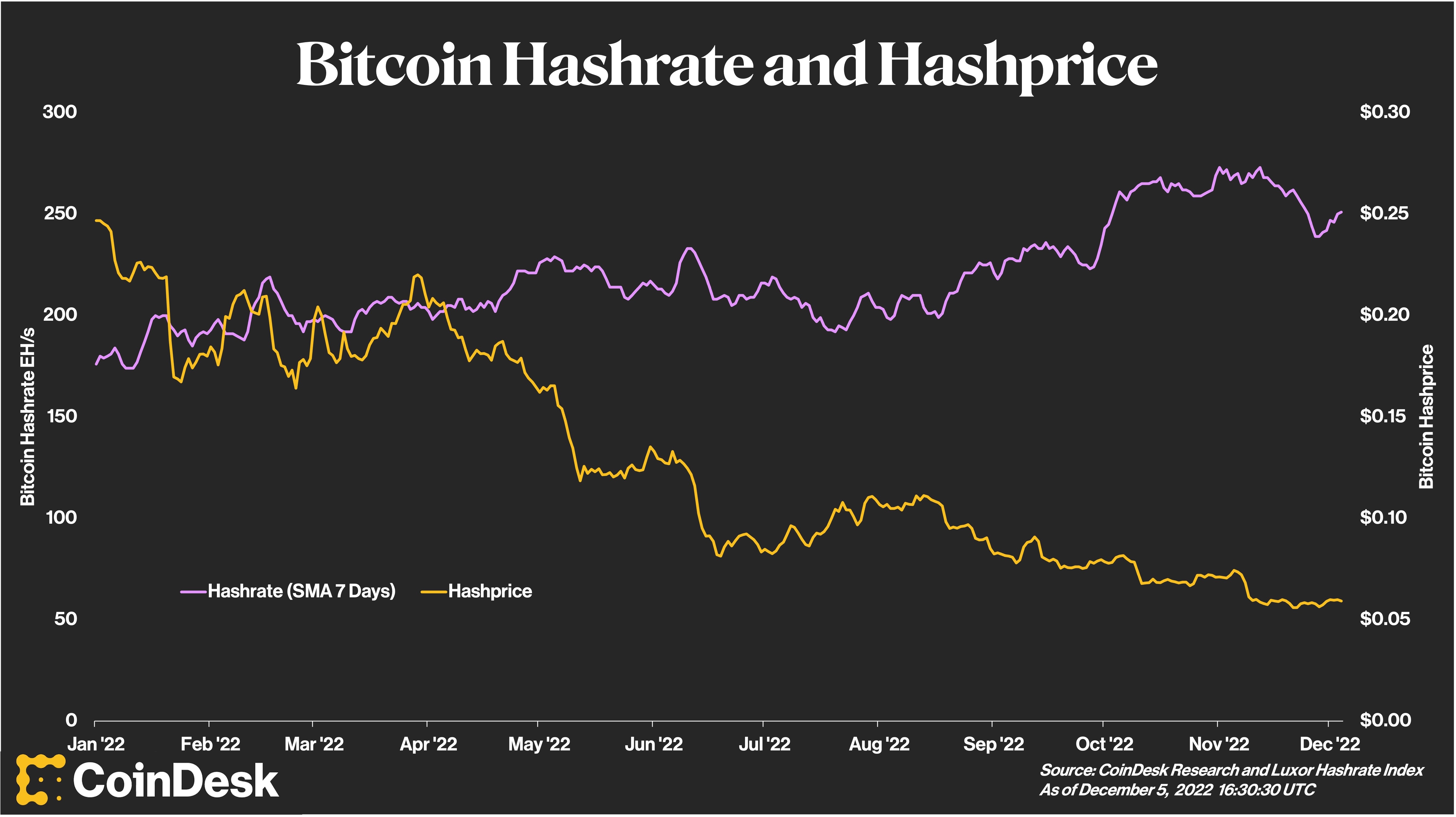

The mining difficulty automatically adjusts according to the hashrate, or computing power, that’s online in order to keep the time it takes to mine a bitcoin block roughly stable: The more miners are working, the higher the difficulty becomes.

In the past several months, bitcoin miners have been caught between a stubbornly low price of bitcoin that decreases their revenue and high electricity rates that increase costs. Major producers like Core Scientific (CORZ) and Argo Blockchain (ARBK) are dealing with liquidity crunches, while Compute North filed for Chapter 11 bankruptcy.

The situation has been exacerbated by new, more efficient machines being delivered and more miners coming online as projects started months ago reached fruition, driving the hashrate higher. Between early August and the last upward adjustment on Nov. 21, the hashrate and difficulty both increased by about one-third.

As the profitability of mining has dropped, the hashrate has continued to increase — until now. (Sage D. Young/CoinDesk Research)

The reality of crypto winter now seems to have caught up with the industry, and bitcoin miners are turning off their machines. The hashrate started dropping around mid-November as profitability took a hit. It is, however, still well above the levels seen after China’s crackdown on the industry.

The profitability of mining has dropped by about 20% in the past month, according to Luxor’s hashprice indicator.

At these “depressed profitability levels, even miners using energy-efficient machines like the Antminer S19j Pro need access to electricity priced lower than $0.08 per kWh,” said Jaran Mellerud, an analyst at Luxor. Even though the average energy price on the network is about $0.05 per kilowatt hour (kWh), many miners are paying about $0.07 – $0.08 per kWh, Mellerud said.

On top of that, energy prices have increased in the last few days, along with the price of natural gas. “Miners buying spot electricity and already operating close to break-even may have seen their electricity prices rise just enough to flip their operations into cash-flow-negative territory,” Mellerud said.

This latest lower hashrate and difficulty doesn’t leave the network more vulnerable to attack. The computing power is spread among five big mining pools and another 12 smaller ones, data from BTC.com shows.